When do trade threats become business reality?

Donald Trump’s announcement that he would impose sweeping tariffs on his first day back in office has jolted trade markets and boardroom planning.

The president-elect’s statement on Truth Social outlined a 25% tariff on all Canadian and Mexican imports until “drugs, in particular Fentanyl, and all Illegal Aliens stop this Invasion of our Country,” alongside an additional 10% tariff on Chinese goods.

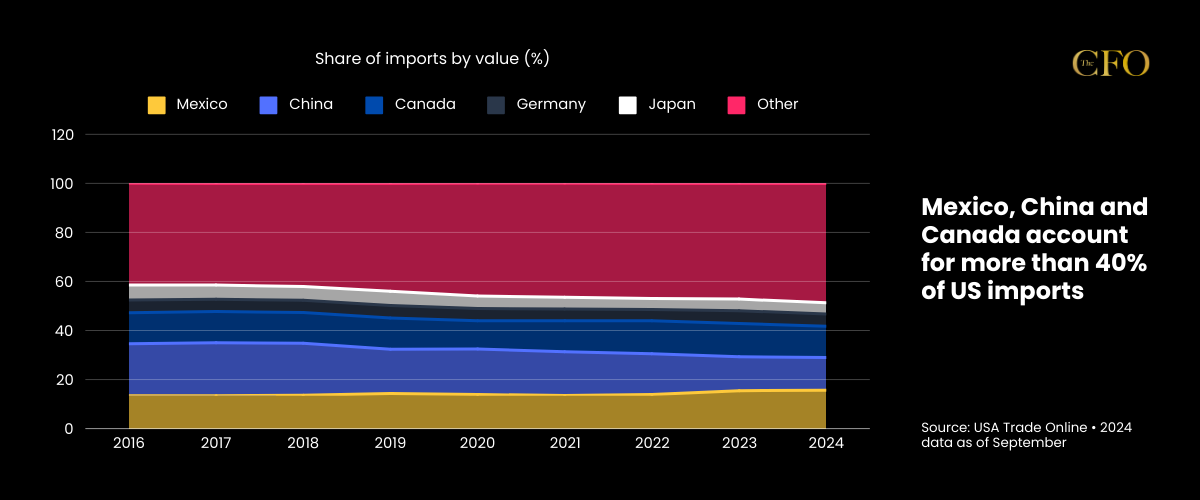

According to Financial Times reporting, these measures would affect 40% of U.S. imports, marking a significant escalation in trade policy that goes beyond previous actions by targeting America’s largest trading partners simultaneously.

While markets have already responded – with the U.S. dollar rising 0.4% and the Mexican peso falling 1.3% – the crucial question for businesses is not if, but when these proposals might materialize into operational realities.

Historical precedents suggest a compressed timeline for implementation. The 2018 steel and aluminum tariffs moved from announcement to implementation in just 15 days, while more complex measures targeting Chinese goods in the same year took effect within 30-45 days. More recently, the Biden administration’s May 2024 tariff increases on Chinese imports, particularly affecting electric vehicles and semiconductors, outlined a 90-day implementation window with a two-year phase-in period.

The scale of integration in North American supply chains adds complexity to any rapid policy shifts. Beyond the widely discussed automotive sector, five key industries face immediate exposure. The aerospace sector operates on deeply established cross-border networks developed under NAFTA and USMCA. Electronics and semiconductor manufacturing has increasingly shifted toward regional integration, while pharmaceutical production shows similar trends toward North American reshoring. Consumer electronics manufacturers and industrial production facilities have also built significant cross-border dependencies.

Economic analysis from previous tariff implementations provides a sobering framework for impact assessment. According to Standard Chartered, historical data shows that a 1% tariff increase on Chinese imports resulted in a 1.5% decline in exports to the U.S. Extrapolating this to the proposed 10% additional tariff suggests potential trade flow disruptions of 15% over a 12-month period. The broader economic implications extend beyond direct trade impacts – previous rounds of tariffs resulted in measurable reductions in real income and job market effects across manufacturing, warehousing, and retail sectors.

The current policy landscape differs significantly from previous trade actions. While earlier measures focused primarily on trade balances and industrial policy, the new proposals explicitly link trade policy to broader security concerns, including immigration control and drug trafficking. This shift in justification could affect both implementation speed and potential modification pathways.

For businesses, the compressed historical timelines for tariff implementation suggest an urgent need for scenario planning. Key considerations include:

The integration of North American trade relationships adds another layer of complexity. Canada’s position as the source of 60% of U.S. crude oil imports highlights the interconnected nature of essential supply chains. Similar dependencies exist across industrial sectors, suggesting that policy implementation may require more nuanced approaches than historical precedents would indicate.

Businesses face a delicate balance between prudent preparation and avoiding overreaction to policy proposals. The historical pattern suggests that while implementation can be rapid, the practical effects often evolve over longer periods as markets adjust and policy details are refined. This suggests a staged approach to response planning, with immediate focus on understanding exposure and developing contingency plans, while maintaining flexibility for longer-term strategic adjustments.

The convergence of policy shifts and market responses requires careful monitoring of both direct impacts and secondary effects. While the immediate focus naturally falls on tariff rates and implementation dates, the broader implications for supply chain restructuring and market repositioning may ultimately prove more significant for long-term business planning.