Revenue Radar: GSK delivers a strong Q2

GSK plc reported robust second-quarter results for 2024, demonstrating continued momentum across its core business areas and prompting an upgrade to its full-year guidance. The company’s performance was driven by strong sales growth and operational execution, despite some challenges in the vaccines segment.

GSK published their results on July 31, 2024.

“GSK’s momentum this year continues with excellent second quarter performance, reflecting strong operational execution and the strengthening breadth of our portfolio to both prevent and treat diseases,” said Emma Walmsley, Chief Executive Officer of GSK.

GSK’s Q2 2024 financial results demonstrate the company’s ability to drive growth while improving profitability. Core operating profit rose 18% to £2.5 billion, outpacing the 13% sales growth and indicating improved operational efficiency. This performance led to a core operating margin of 31.9%, up 1.3 percentage points year-over-year, reflecting the company’s focus on cost management and portfolio optimization.

The company’s core earnings per share (EPS) increased by 13% to 43.4p, aligning closely with overall sales growth. This suggests that GSK is successfully translating top-line growth into shareholder value, despite ongoing investments in research and development and commercial activities.

Free cash flow for the quarter stood at £328 million, demonstrating GSK’s ability to generate substantial cash from its operations. This strong cash generation provides the company with flexibility to invest in its pipeline, pursue strategic opportunities, and return value to shareholders.

GSK continues to invest significantly in research and development, with R&D expenses increasing by 9% in the quarter. This investment is crucial for maintaining the company’s pipeline and future growth prospects. Key areas of focus include respiratory diseases, HIV, and oncology, with several promising candidates in late-stage development.

Notable pipeline progress in Q2 2024 included:

“I am confident in our underlying business momentum, but obviously, the second-half growth rates are very different from the first, with the second half significantly impacted by the very strong launches of Arexvy and in Oncology last year, as well as initial stock builds,” said CFO, Julie Brown.

The company also made strategic moves to enhance its technological capabilities and pipeline. This included the acquisition of Aiolos Bio to strengthen its respiratory pipeline and a restructured collaboration with CureVac to gain full control of candidate mRNA vaccines.

“In the past 6 months, we have secured regulatory approvals, or received acceptance of submissions for 10 major medicines and vaccines and reported positive data from 7 phase III studies, clearly demonstrating the innovation and health impact that GSK is now bringing to patients,” said Tony Wood, Chief Scientific Officer.

Despite these positive developments, GSK faces ongoing challenges, particularly in its vaccines business. The company is navigating complex dynamics in the US market for Shingrix and dealing with regulatory hurdles for its RSV vaccine Arexvy. The postponement of an ACIP vote for Arexvy in the 50-59 age group highlights the uncertainties inherent in the vaccine approval and recommendation process.

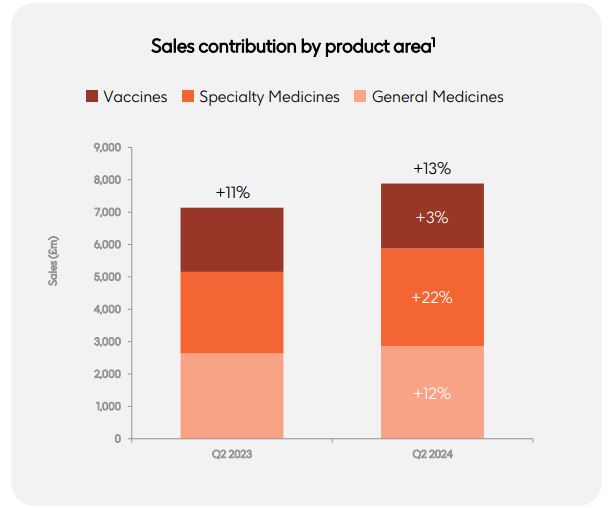

GSK’s Q2 2024 results reveal a complex picture of growth and challenges across its diverse portfolio. Specialty Medicines emerged as a standout performer, with sales surging 22% to £3.024 billion, underscoring GSK’s successful pivot towards innovative, high-value treatments.

Within this segment, the HIV business showed robust growth of 13%, propelled by increased demand for long-acting treatments, reflecting evolving patient preferences. Even more impressive was the Oncology division, where sales more than doubled to £356 million, highlighting GSK’s rapidly expanding footprint in the lucrative cancer treatment market.

The Vaccines segment, however, presented a mixed picture. Overall growth was modest at 3% (excluding COVID-19 solutions), reaching £1.999 billion. This performance was tempered by challenges faced by Shingrix, GSK’s shingles vaccine, which saw a 4% decline in sales to £832 million.

The company attributed this downturn to issues in the US market, including channel inventory reductions, changes in retail vaccine prioritization, and difficulties in activating harder-to-reach consumers. On a brighter note, meningitis vaccines demonstrated strong growth of 24%, indicating GSK’s ability to capitalize on specific market opportunities within its vaccines portfolio.

Surprisingly, General Medicines outperformed expectations with 12% growth to £2.861 billion. This performance was primarily driven by Trelegy, a respiratory drug that saw exceptional 41% growth. The strong showing in General Medicines suggests that GSK’s established products continue to hold significant value and growth potential, contrary to concerns about patent expirations and generic competition.

These varied outcomes across segments reflect GSK’s evolving portfolio strategy and the complex market dynamics it faces. The shift towards specialty and innovative treatments is clearly paying off, as evidenced by strong growth in Specialty Medicines and Oncology. However, challenges in the US vaccine market, particularly for Shingrix, highlight the need for adaptive marketing strategies and potential reassessment of growth expectations in this area.

“In Q2 2024 and YTD, sales growth increased primarily driven by Trelegy, a chronic obstructive pulmonary disease (COPD) and asthma medicine, with strong demand across all regions and pricing benefits from channel and segment mix and adjustments to returns and rebates in the US,” said Luke Miels, Chief Commercial Officer.

GSK’s strong performance in Q2 2024 has led the company to upgrade its full-year guidance, demonstrating confidence in its growth trajectory and operational execution. The revised outlook reflects the company’s ability to navigate challenges while capitalizing on strengths across its portfolio.

For the full year 2024, GSK now expects:

These projections exclude any contributions from COVID-19 solutions and are provided at constant exchange rates.

“GSK continues to anticipate an increase in the Core effective tax rate to around 17% for the full year following implementation of new global minimum corporate income tax rules which came into effect from 1 January 2024 in line with the Organisation for Economic Co-Operation and Development ‘Pillar 2’ model framework,” said CFO, Julie Brown.

The company also revised its turnover expectations for individual segments:

“With our current momentum, and the continued progress we are making, we have today upgraded our outlook for 2024, demonstrating the strengthening depth and breadth of our portfolio,” said Walmsley.

The upgraded guidance for Specialty Medicines and General Medicines reflects the strong performance and positive momentum in these areas. However, the downward revision for Vaccines highlights the challenges faced in this segment, particularly with Shingrix in the US market and the evolving landscape for the RSV vaccine Arexvy.

Looking beyond 2024, GSK maintains its medium and long-term outlooks:

Importantly, these long-term projections do not yet include potential contributions from Blenrep or ongoing progress in the early-stage pipeline, suggesting potential upside to these targets.

See GSK’s full investor deck here: GSK PowerPoint template