The hidden red flags in Alphabet's most recent earnings

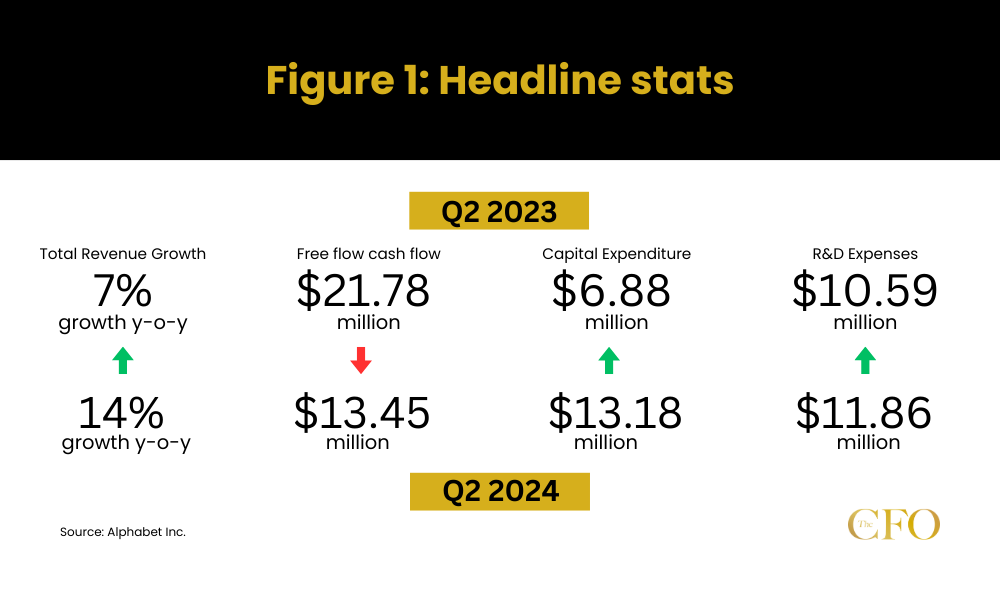

Alphabet Inc., Google’s parent company, reported a strong second quarter for 2024, with revenues climbing 14% year-over-year to $84.7 billion. The tech giant’s core search business continued to show resilience, while Google Cloud finally crossed the $10 billion quarterly revenue threshold.

“Our strong performance this quarter highlights ongoing strength in Search and momentum in Cloud,” said Sundar Pichai, CEO of Alphabet and Google. “We are innovating at every layer of the AI stack.”

However, beneath the surface of these impressive figures, several red flags suggest that Alphabet may face significant challenges in the coming months. From increasing competitive pressures to potential monetization hurdles for its AI initiatives, Google’s dominance in the tech landscape may be under threat.

While Google’s search revenue grew by 14% year-over-year to $48.5 billion, the company faces a looming threat from AI-powered competitors. The imminent launch of Nvidia’s Blackwell platform in early 2025 could empower rivals to create more sophisticated search alternatives, potentially eroding Google’s market share.

Google’s response to this challenge – AI-powered search features like AI Overviews – comes with its own set of problems. Pichai noted, “We are relentlessly driving efficiencies in our AI models,” but these efficiencies may not be enough to offset the increased costs associated with AI-powered search.

The company’s CFO, Ruth Porat, hinted at the financial implications of this shift, stating, “As we invest to support our highest growth opportunities, we remain committed to creating investment capacity with our ongoing work to durably re-engineer our cost base.”

This statement suggests that Google is bracing for a period of higher costs and potentially lower margins as it transitions to more AI-intensive search capabilities. The challenge lies in maintaining profitability while delivering the advanced features necessary to fend off emerging competitors.

Moreover, the monetization model for AI-powered search remains unclear. Traditional search relies heavily on sponsored links and ads, but integrating these seamlessly into AI-generated responses presents a significant challenge. Google may need to explore alternative revenue models, such as subscriptions or premium features, which could face resistance from users accustomed to free search services.

YouTube, historically a strong performer in Alphabet’s portfolio, showed signs of vulnerability in Q2 2024. While YouTube ad revenues grew by 13% year-over-year to $8.7 billion, this growth rate lagged behind that of Google Search, indicating potential challenges in the video platform’s monetization strategy.

Philipp Schindler, Google’s Chief Business Officer, attempted to paint a positive picture, stating, “YouTube is focused on a clear strategy: connecting creators with a massive audience, and enabling them to build successful businesses through ads and subscriptions.” However, the details revealed a more complex situation.

Brand advertising, typically a strong driver for YouTube, showed weakness. Schindler noted that YouTube’s growth was “driven by growth in brand, as well as direct response,” but the emphasis on direct response advertising suggests that big-budget brand campaigns may be pulling back.

This shift could be indicative of broader changes in the advertising landscape. As consumers increasingly use platforms like TikTok and Instagram for product discovery, advertisers may be reallocating their budgets away from traditional YouTube ads.

Furthermore, YouTube faces challenges in its content strategy. The company’s investment in YouTube Shorts, its short-form video offering, has yet to fully pay off. Pichai mentioned that “views of YouTube Shorts on connected TVs more than doubled last year,” but failed to provide concrete monetization figures for this format.

The recent addition of NFL Sunday Ticket to YouTube TV, while potentially attractive to subscribers, represents a significant content cost that could pressure margins in the short term. The company’s ability to monetize this expensive sports rights package effectively will be crucial for YouTube’s future profitability.

Lastly, Google’s decision to retain third-party cookies, announced just before the earnings call, suggests that the company’s efforts to develop privacy-preserving alternatives have not yielded satisfactory results. This could impact YouTube’s ability to deliver targeted advertising effectively in the future, potentially further eroding its appeal to advertisers.

At first glance, Google Cloud’s performance in Q2 2024 appears impressive. The division crossed two significant milestones, generating over $10 billion in quarterly revenue for the first time and achieving $1 billion in quarterly operating profit. Pichai celebrated this achievement, stating, “Cloud reached some major milestones. Quarterly revenues crossed the $10 billion mark for the first time, and at the same time passed the $1 billion mark in quarterly operating profit.”

However, a closer examination reveals potential concerns lurking beneath these headline figures. Despite its growth, Google Cloud remains a distant third in the cloud computing race, significantly behind market leaders Amazon Web Services (AWS) and Microsoft Azure.

The competitive landscape in cloud services is intensifying, particularly in the realm of AI-powered offerings. While Pichai noted that “AI Infrastructure and Generative AI Solutions for Cloud customers have already generated billions in revenues,” he didn’t provide specific figures or growth rates for these services. This lack of detail raises questions about the actual impact of AI on Cloud’s bottom line.

Moreover, Google’s approach to AI in the cloud appears to be playing catch-up. Pichai mentioned, “We broadened support for third-party models, including Anthropic’s Claude 3.5 Sonnet, and open source models like Gemma 2, Llama and Mistral.” This strategy of supporting multiple AI models, while potentially appealing to customers, could also be seen as a lack of confidence in Google’s own AI offerings.

The pressure to compete in AI capabilities may also squeeze Google Cloud’s newly achieved profitability. Porat cautioned, “Looking ahead in Q3, we do expect the same seasonal pattern that you saw last year with respect to margin, and we are continuing to invest in the business.” This suggests that the $1 billion profit milestone may not be sustained in the coming quarters as Google ramps up investment to stay competitive.

Furthermore, Google’s late entry into the generative AI race for enterprise customers could prove costly. While the company touts its AI infrastructure and Vertex AI platform, it lacks the first-mover advantage enjoyed by competitors like Microsoft, which has deeply integrated OpenAI’s technology across its cloud services.

As the cloud market matures and competition intensifies, Google may find it increasingly difficult to differentiate its offerings and maintain growth rates without sacrificing profitability. The coming quarters will be crucial in determining whether Google Cloud can truly establish itself as a formidable competitor in the enterprise cloud market or if it will remain perpetually in third place.

Alphabet’s commitment to artificial intelligence was a recurring theme throughout the earnings call, with Pichai emphasising the company’s efforts to “innovate at every layer of the AI stack.” However, the details provided suggest that Google’s AI initiatives may be more costly and less immediately impactful than investors might hope.

Pichai highlighted the deployment of Gemini, Google’s latest AI model, across the company’s products: “All six of our products with more than 2 billion monthly users now use Gemini.” Yet, the tangible benefits of this integration remain unclear. While Pichai mentioned increased user engagement with AI-powered features like AI Overviews in Search, he provided no specific metrics on how these features are driving revenue growth.

The company’s AI infrastructure investments are substantial. Pichai introduced Trillium, the sixth generation of Google’s custom AI accelerator, boasting significant performance improvements. However, these advancements come at a cost. Ruth Porat warned of “increases in depreciation and expenses associated with the higher levels of investment in our technical infrastructure” in the coming quarter, suggesting that the full financial impact of Google’s AI push is yet to be felt.

Moreover, Google’s approach to AI monetization appears cautious and potentially behind competitors. Philipp Schindler’s comments on AI in advertising focused primarily on incremental improvements to existing ad products rather than revolutionary new offerings. He noted, “This quarter we announced over 30 new Ads features and products to help advertisers leverage AI,” but many of these seemed to be enhancements to existing tools rather than ground-breaking innovations.

The company’s enterprise AI offerings also face challenges. While Pichai mentioned that “more than 1.5 million developers are now using Gemini across our developer tools,” he provided no information on how this translates to revenue. The lack of concrete financial metrics for AI-driven products and services raises questions about their current profitability and future potential.

Furthermore, Google’s AI strategy appears somewhat scattered. The company is pursuing multiple AI initiatives across various product lines, from search to cloud to workspace applications. This broad approach, while potentially covering all bases, may also dilute focus and resources, potentially allowing more specialized competitors to gain advantages in specific areas.

As the AI race intensifies, Google faces the dual challenge of justifying its massive investments in AI technology while also finding ways to effectively monetize these advancements. The coming quarters will be crucial in determining whether Google’s AI bet will pay off or if the costs will outweigh the benefits in the near term.