Banking » Revenue Radar: Banking update as Citi, BNY Mellon, Wells Fargo and JP Morgan report

Revenue Radar: Banking update as Citi, BNY Mellon, Wells Fargo and JP Morgan report

The second quarter of 2024 presented a complex operating environment for major U.S. banks, characterised by economic uncertainty, geopolitical tensions, and evolving regulatory landscapes. Despite these challenges, JPMorgan Chase, Citigroup, Wells Fargo, and BNY Mellon all reported solid financial results, demonstrating the resilience and adaptability of their business models.

JPMorgan Chase led the pack with exceptional performance, reporting a 25% year-over-year increase in net income to $18.1 billion. This impressive growth was partly attributable to a $7.9 billion net gain related to Visa shares, but even excluding this one-time item, the bank’s core businesses showed strong momentum. CEO Jamie Dimon noted, “The Firm performed well in the second quarter, generating net income of $13.1 billion and a ROTCE of 20% after excluding a net gain on our Visa shares, a contribution to the Firm’s Foundation and discretionary securities losses.”

Citigroup also posted robust results, with net income rising 10% year-over-year to $3.2 billion. The bank’s performance was driven by growth across all business segments, particularly in Banking and Markets. CEO Jane Fraser commented, “Our second quarter results show the progress we are making in executing our strategy and the benefit of our diversified business model.”

Wells Fargo’s performance was more subdued, with net income declining slightly by 1% year-over-year to $4.9 billion. However, the bank showed resilience in the face of continued regulatory constraints and legacy issues. CEO Charlie Scharf stated, “Our efforts to transform Wells Fargo were reflected in our second quarter financial performance as diluted earnings per common share grew from both the first quarter and a year ago.”

BNY Mellon rounded out the group with a solid 9% year-over-year increase in net income to $1.2 billion. The bank’s focus on fee-based revenues and expense management yielded positive results. CEO Robin Vince remarked, “BNY Mellon delivered another quarter of improved financial performance, with positive operating leverage on the back of solid fee growth and continued expense discipline.”

A common thread among all four banks was the pressure on net interest income due to rising deposit costs, offset to varying degrees by growth in fee-based revenues and trading income. The banks also emphasized their strong capital positions, with most announcing dividend increases, reflecting confidence in their ability to navigate the current economic environment.

Financial Performance Comparison

The second quarter of 2024 saw varied financial performances across JPMorgan Chase, Citigroup, Wells Fargo, and BNY Mellon, reflecting their diverse business models and strategic priorities.

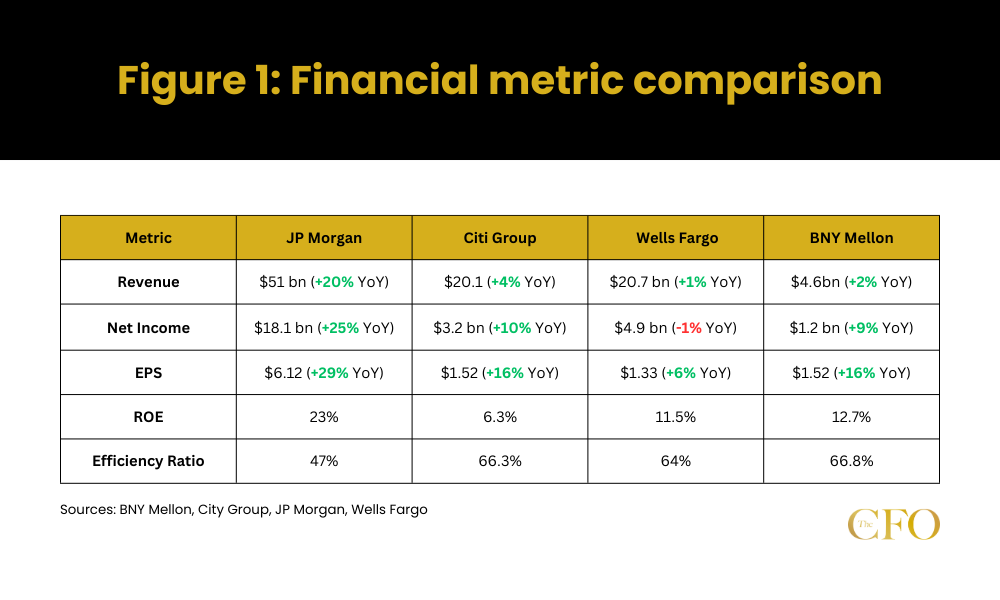

JPMorgan Chase stood out with exceptional results, reporting a 20% year-over-year increase in revenue to $51.0 billion and a 25% rise in net income to $18.1 billion. However, it’s crucial to note that these figures include a significant $7.9 billion net gain related to Visa shares. Even when excluding this one-time item, the bank’s performance was impressive. JPMorgan’s earnings per share (EPS) of $6.12 represented a 29% increase from the previous year, while its return on equity (ROE) reached a remarkable 23%.

Citigroup demonstrated solid growth, with revenue increasing by 4% year-over-year to $20.1 billion and net income rising 10% to $3.2 billion. The bank’s EPS of $1.52 marked a 16% improvement from the previous year. However, Citigroup’s ROE of 6.3% lagged behind its peers, reflecting ongoing challenges in some areas of its business.

Wells Fargo’s performance was more subdued, with revenue growing modestly by 1% year-over-year to $20.7 billion and net income declining slightly by 1% to $4.9 billion. Despite this, the bank managed to increase its EPS by 6% to $1.33, partly due to share repurchases. Wells Fargo’s ROE of 11.5% showed improvement from the previous year but remained below pre-pandemic levels.

BNY Mellon, despite its smaller size, delivered solid results with a 2% year-over-year increase in revenue to $4.6 billion and a 9% rise in net income to $1.2 billion. The bank’s EPS of $1.52 represented a 16% increase from the previous year, matching Citigroup’s growth rate. BNY Mellon’s ROE of 12.7% was competitive within the group.

A key metric to consider is the efficiency ratio, which measures a bank’s ability to generate revenue from its expenses. JPMorgan Chase led the pack with an impressive 47% efficiency ratio, indicating strong cost management. Wells Fargo followed with 64%, while Citigroup and BNY Mellon had similar ratios of 66.3% and 66.8% respectively, suggesting room for improvement in operational efficiency.

It’s worth noting the divergence in net interest income (NII) performance across the banks. Wells Fargo reported a 9% year-over-year decline in NII, reflecting pressure from higher deposit costs and lower loan balances. Citigroup saw a modest 3% increase, while JPMorgan Chase reported a 4% rise in NII. BNY Mellon, with its different business model, experienced a 6% decrease in NII.

These variations in NII performance underscore the importance of diversified revenue streams in the current economic environment. JPMorgan Chase CEO Jamie Dimon highlighted this point, stating, “We continued to see growth in our fee-based revenue offsetting an expected decline in net interest income.”

The banks’ performances also reflected their varying exposures to different business segments. JPMorgan Chase and Citigroup benefited from strong trading and investment banking revenues, while Wells Fargo’s results were buoyed by growth in credit card spending and account growth. BNY Mellon’s performance was driven by higher asset servicing and clearing fees.

Business Segment Analysis

Consumer Banking

In the consumer banking space, JPMorgan Chase continued to demonstrate strength. The bank’s Consumer & Community Banking segment reported a 3% year-over-year increase in revenue to $17.7 billion. This growth was primarily driven by a 14% increase in Card Services & Auto revenue, reflecting higher net interest income on increased revolving balances and higher card income from increased sales volume. However, the segment’s net income decreased by 21% to $4.2 billion, largely due to a higher provision for credit losses.

Citigroup’s U.S. Personal Banking division also showed robust performance, with revenues increasing by 6% year-over-year to $4.9 billion. All three businesses within this segment – Branded Cards, Retail Services, and Retail Banking – contributed to the top-line growth. However, like JPMorgan Chase, Citigroup saw a significant increase in its cost of credit in this segment, leading to a 74% decrease in net income to $121 million.

Wells Fargo’s Consumer Banking and Lending segment presented a mixed picture. While the segment’s revenue increased by 3% year-over-year, net income decreased by 7% to $1.8 billion. The bank reported strong growth in credit card spending and new account openings, with CEO Charlie Scharf noting, “We have now launched nine new cards since 2021, driving strong credit card spend and account growth.”

Investment Banking and Markets

Investment banking and trading activities were significant drivers of performance for several banks in the quarter. JPMorgan Chase’s Corporate & Investment Bank segment delivered outstanding results, with total revenue up 9% year-over-year to $17.9 billion. The bank reported a 46% increase in Investment Banking revenue and a 10% rise in Markets revenue. CEO Jamie Dimon highlighted, “In the CIB, investment banking fees rose 50%, albeit against a low base, and our market share improved across products to 9.5% YTD.”

Citigroup also saw strong performance in this area. The bank’s Markets revenues increased by 6% year-over-year to $5.1 billion, driven by a 37% increase in Equity markets revenue. Investment Banking revenues surged by 60% to $853 million, benefiting from increased activity across Debt Capital Markets, Equity Capital Markets, and Advisory services.

Wells Fargo, with its more limited presence in investment banking, reported a 50% year-over-year increase in investment banking fees, although from a smaller base compared to its peers.

Wealth and Asset Management

In the wealth and asset management space, results were generally positive but showed some variation. JPMorgan Chase’s Asset & Wealth Management segment reported a 6% year-over-year increase in revenue to $5.3 billion, driven by growth in management fees on higher average market levels and strong net inflows.

Citigroup’s Wealth segment saw a modest 2% year-over-year increase in revenues to $1.8 billion, with higher investment fee revenues partially offset by lower net interest income. The bank reported a 15% year-over-year increase in client investment assets to $540 billion.

BNY Mellon’s Investment and Wealth Management segment reported a slight 1% year-over-year increase in revenue to $821 million. The bank’s assets under management (AUM) grew by 7% year-over-year to $2.05 trillion, benefiting from higher market values and net inflows.

Corporate and Commercial Banking

In corporate and commercial banking, results were mixed. JPMorgan Chase’s Commercial Banking segment saw a 7% year-over-year decrease in revenue to $3.1 billion, primarily due to lower net interest income. However, the bank reported continued momentum in payments and cross-border business.

Citigroup’s Services segment, which includes Treasury and Trade Solutions and Securities Services, reported a 3% year-over-year increase in revenues to $4.7 billion. The bank highlighted strong underlying fee growth and increased activity in cross-border payments.

Wells Fargo’s Commercial Banking segment saw a slight 1% year-over-year decrease in average loans, but reported growth in treasury management fees.

Balance Sheet and Capital

Loans and Deposits

Loan growth was mixed across the four banks, reflecting differing strategic priorities and market conditions. JPMorgan Chase reported a 6% year-over-year increase in average loans, driven primarily by growth in credit card balances and strength in wholesale lending. CEO Jamie Dimon noted, “We continue to invest heavily into our businesses for long-term growth and profitability.”

Citigroup saw a 4% year-over-year increase in end-of-period loans, with growth particularly strong in the bank’s Markets and Services segments. Wells Fargo, however, reported a 3% year-over-year decline in average loans, primarily due to lower balances in its commercial real estate portfolio. BNY Mellon bucked the trend with a significant 8% year-over-year increase in average loans, albeit from a smaller base than its universal banking peers.

On the deposit front, the picture was similarly varied. JPMorgan Chase and Wells Fargo both reported relatively flat year-over-year deposit balances, while Citigroup saw a 3% decline. BNY Mellon, in contrast, reported a 3% year-over-year increase in average deposits. These trends reflect ongoing shifts in consumer and business liquidity preferences, as well as the impact of quantitative tightening by central banks.

Wells Fargo CFO Mike Santomassimo commented on the deposit environment, stating, “We continued to see growth in deposit balances in all of our businesses, and the pace of customers reallocating cash into higher yielding alternatives slowed.”

Capital Position and Ratios

All four banks maintained strong capital positions, with Common Equity Tier 1 (CET1) ratios well above regulatory requirements. JPMorgan Chase led the group with a CET1 ratio of 15.3%, up significantly from 13.4% a year ago. Citigroup followed with a CET1 ratio of 13.6%, while Wells Fargo and BNY Mellon reported ratios of 11.0% and 11.4% respectively.

These robust capital positions enabled the banks to continue returning capital to shareholders through dividends and share repurchases. JPMorgan Chase announced a 5% increase in its quarterly common stock dividend to $1.15 per share. Wells Fargo plans to increase its third-quarter common stock dividend by 14%, subject to board approval. Citigroup raised its quarterly dividend by 6% to $0.53 per share, and BNY Mellon increased its quarterly dividend by 12% to $0.42 per share.

Share repurchases also continued, albeit at a more measured pace than in previous years. JPMorgan Chase repurchased $4.9 billion of common stock during the quarter, while Citigroup repurchased $1 billion worth of shares. Wells Fargo repurchased $6.1 billion of common stock, and BNY Mellon repurchased $601 million of shares.

Liquidity and Funding

The banks maintained strong liquidity positions, with high-quality liquid assets (HQLA) and liquidity coverage ratios (LCR) well above regulatory minimums. JPMorgan Chase reported $1.5 trillion in cash and marketable securities, underlining its fortress balance sheet approach. BNY Mellon reported an average LCR of 115% and an average net stable funding ratio (NSFR) of 132%, both comfortably above regulatory requirements.

Citigroup’s CEO Jane Fraser emphasised the bank’s strong balance sheet position, stating, “Our second quarter results showcased the strength of our balance sheet. Our CET1 ratio now stands at 13.6%.”

Outlook and Guidance

All four banks acknowledged the complex and uncertain economic environment they are operating in.

JPMorgan Dimon provided perhaps the most comprehensive outlook. “The geopolitical situation remains complex and potentially the most dangerous since World War II — though its outcome and effect on the global economy remain unknown,” he said.

He further noted, “There has been some progress bringing inflation down, but there are still multiple inflationary forces in front of us: large fiscal deficits, infrastructure needs, restructuring of trade and remilitarisation of the world.” This cautious sentiment was echoed by the other banks. Citigroup’s Fraser mentioned that while the bank is pleased with its progress, it remains “focused on running our company better and the hard work ahead.” Wells Fargo’s CEO Charlie Scharf noted that while credit performance was consistent with their expectations, “commercial loan demand remained tepid.”

Interest Rates and Net Interest Income

The outlook for interest rates and their impact on net interest income (NII) was a key focus. JPMorgan Chase raised its full-year NII guidance to $87 billion, excluding Markets, reflecting the bank’s expectation of a continued favourable rate environment. However, Dimon cautioned that “inflation and interest rates may stay higher than the market expects.”

Wells Fargo, which had seen pressure on NII, expects this trend to continue. Scharf noted, “We continued to see growth in our fee-based revenue offsetting an expected decline in net interest income.”

BNY Mellon expressed optimism about the interest rate environment, with CEO Robin Vince stating the bank “expects continued benefits from higher interest rates and expense management.”

Credit Quality

The banks generally expressed confidence in current credit quality but remained vigilant about potential future deterioration. JPMorgan Chase increased its reserve for credit losses, particularly in the credit card portfolio, reflecting growth and updates to certain macroeconomic variables. Wells Fargo reported that credit performance was consistent with expectations, while Citigroup noted higher net credit losses, particularly in cards, as newer vintages season and credit normalisation continues.

Business Segment Outlook

In terms of business segments, investment banking and trading activities are expected to remain strong, benefiting from increased market activity and volatility. JPMorgan Chase and Citigroup both highlighted improved investment banking pipelines and continued strength in trading revenues.

Consumer banking outlooks were mixed, with growth expected in credit card spending and balances, but potential pressure from higher deposit costs and a slowdown in mortgage activity.

Wealth and asset management businesses are anticipated to benefit from higher market values and continued client inflows, although margin pressure from higher deposit costs remains a concern.

All banks emphasised their continued focus on expense management and operational efficiency. Citigroup’s Fraser stated, “We are modernising our infrastructure to improve our client service and automating processes to strengthen controls.” BNY Mellon’s Vince highlighted the bank’s “continued expense discipline” as a key driver of improved financial performance.

The banks also acknowledged the evolving regulatory landscape. JPMorgan Chase noted that it now has “excess capital even after the uncertainty created by Basel III endgame,” referring to upcoming changes in regulatory capital requirements.

While the major banks expressed cautious optimism about their ability to navigate the current economic environment, they also acknowledged significant uncertainties ahead. Key themes in their outlooks included the potential for persistently higher inflation and interest rates, the importance of expense management, and the need to remain vigilant about credit quality. Despite these challenges, the banks generally projected confidence in their strategic directions and their ability to deliver value to shareholders in the coming quarters.