Risk & Economy » Compliance » Understanding Right-of-Use Assets and Lease Liabilities under FRS 102

Understanding Right-of-Use Assets and Lease Liabilities under FRS 102

Lease accounting under FRS 102 continues to challenge finance teams. From discount rate selection to right-of-use asset measurement, this guide explores the key differences from IFRS 16 and how finance leaders can build clarity, compliance, and confidence into their reporting.

Lease accounting is one of the more intricate areas of financial reporting, where compliance and clarity intersect. UnderFRS 102, right-of-use (ROU) assets and lease liabilities must be measured and reported with care. While the principles share similarities with IFRS 16, important differences in the treatment continue to demand attention from finance leaders.

Initial measurement

At the outset, the lease liability is recorded at the present value of future lease payments. Discounting requires the use of either the obtainable borrowing rate (OBR) or, if that is not available, the incremental borrowing rate (IBR). The ROU asset is recognised at the amount of the lease liability, adjusted for any initial direct costs, lease incentives, and prepayments.

This process is rarely straightforward. Lease agreements often contain features such as indexation or market-linked adjustments that influence the cash flows to be included. Determining which elements to capture requires careful judgement and close review of contractual terms. Errors made here can ripple forward, affecting both depreciation charges and reported liabilities in later years. ICAEW’s technical helpsheeton leases under FRS 102 provides further guidance.

An overstatement of the ROU asset, for example, distorts future depreciation. Understatement of the liability may lead to covenant risk if lenders view the balance sheet as carrying less debt than is truly the case. For this reason, initial measurement is more than an accounting exercise: it sets the foundation for reliable reporting.

Subsequent measurement

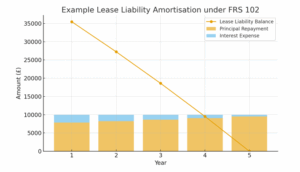

Once on the books, the lease liability grows with interest expense and declines as payments are made. The ROU asset, by contrast, is typically depreciated on a straight-line basis. This mismatch creates a front-loaded expense pattern that shows heavier charges in the early years of a lease.

Interest is highest at the start of the lease, when the liability is largest. Over time, as repayments reduce the liability, the interest portion declines, leaving depreciation as the steady component. The combined effect is a shifting expense profile that has implications for earnings forecasts and performance analysis.

A simple amortisation schedule illustrates the dynamic: interest falls year by year,while principal repayment increases, even as the total payment remains level. This change in mix matters for stakeholders reviewing earnings trajectories and assessing how operating expenses evolve over time.

OBR versus IBR

Selecting the appropriate discount rate remains one of the most challenging judgements in lease accounting. The obtainable borrowing rate reflects the rate at which an entity could borrow funds from a lender to acquire an asset of similar value, with similar security, over a comparable term. The incremental borrowing rate, in contrast, represents an estimate made in the absence of observable data.

Where the OBR can be identified, it is generally more accurate. Yet in practice, many entities default to the IBR, which introduces variation across reporting and can increase the likelihood of audit challenge. The distinction is not academic. A shift of only a few basis points can materially alter the valuation of lease liabilities.

Consider a lease portfolio valued at £10 million. Discounting at 3% produces a liability of roughly £8.5 million, while applying a 5% discount rate reduces that figure closer to £7.7 million. The £800,000 difference flows through to depreciation, interest charges, leverage ratios, and covenant compliance. Documentation and transparency around the choice of rate are essential if reported figures are to stand up to scrutiny.

The impact of ROU asset and liability measurement extends well beyond technical compliance. Reported EBITDA, leverage metrics, and investor communications are all influenced by lease accounting. Research from the ICAEW shows that approximately 40% of finance leaders cite lease accounting as one of the three most complex aspects of FRS 102 compliance. Discount rate assumptions are a common source of material misstatement.

EBITDA in particular is affected. Lease interest is presented below the EBITDA line, while depreciation sits in operating costs. The combined effect can lift EBITDA compared with previous standards, even when no change in operational performance has occurred. Analysts and investors who are unaware of this shift may draw incorrect conclusions if disclosures do not explain the accounting mechanics clearly.

Borrowing capacity and covenants also come into play. Higher lease liabilities inflate debt-like obligations, which can raise leverage ratios. For companies with tight covenant headroom, the accounting treatment of leases may directly affect access to capital markets. Transparent communication with lenders and investors is therefore critical in ensuring that financial reporting is understood in context.

Systems and governance

As reporting requirements evolve, the ability to capture and model discount rates accurately has become increasingly important. While spreadsheets remain a common tool, they carry limitations in scale, error risk, and auditability. Larger or more complex lease portfolios often demand more sophisticated solutions.

Automating lease accounting through dedicated software platforms can deliver consistency, reduce errors, and create the audit trail regulators expect. Integration with general ledgers, automated disclosure reports, and sensitivity modelling are among the features that can transform compliance from a manual exercise into a streamlined process.

Governance is equally important. Clear policies on rate selection, periodic reviews of methodologies, and the use of market benchmarks all help to reduce risk. Training finance teams to recognise the nuances of FRS 102ensures that knowledge is embedded rather than concentrated in a few individuals.

Conclusion

Right-of-use assets and lease liabilities are not simply technical calculations. They influence performance metrics, borrowing capacity, and investor perception. Robust measurement and transparent disclosure under FRS 102 are essential for financial clarity.

With ongoing regulatory attention to discount rate assumptions and reporting practices, the combination of rigorous methodology and reliable automation provides both compliance assurance and strategic benefit. When properly managed, lease accounting becomes not just a reporting requirement but a foundation for more confident decision-making.

To find out more about the changes to lease accounting under FRS 102 and the steps businesses should take to streamline compliance, read this guide.