Risk & Economy » Trade » Why CFOs are betting the house on themselves (and what international tripwires to watch)

Why CFOs are betting the house on themselves (and what international tripwires to watch)

The latest Deloitte CFO Signals survey reveals a stunning confidence gap: finance leaders are optimistic about their own companies but wary of the world. We analyze the investment window opening with potential Fed cuts and detail the Q4 tripwires, from talent wars to global tariffs that demand a decisive strategy.

For months, the North American CFO has been flying blind, strapped into an economy that felt like a perpetually turbulent flight. Now, the latest data suggests the pilot light has flickered back on.

The Deloitte CFO Signalssurvey for Q3 reveals that US finance leaders are experiencing an extraordinary decoupling of confidence: they remain deeply skeptical of the broader economic weather yet are practically euphoric about their own companies’ ability to thrive. This isn’t just a mood swing; it’s the crucial psychological shift needed for meaningful capital allocation, and it’s why Q4 is set to be a period of decisive action or painful regret.

The Fuel Injection: Own-Company Optimism Soars

The headline is clear: The aggregate CFO confidence score ticked up to 5.7 (medium territory) from 5.4. A modest rise, perhaps, but its true significance lies in what the finance chiefs are saying about their own organizations.

Consider the data: A mind-boggling 90% of CFOs now say their company’s financial prospects are “much better or better” than they were three months ago. That’s more than double the 48% recorded in the prior quarter. For the stewards of corporate strategy, this is the equivalent of moving from a defensive crouch to a sprinter’s starting block.

Why is this sudden surge of internal optimism so vital? Because, as David Reichert, Director of International Expansion Solutions at Vistra, argues, confidence isn’t a vanity metric. It’s the fuel for the engine of growth.

“This shift in sentiment is critical if we’re to see sustained growth,” Reichert comments. “While tariffs and economic policy will likely stay in a cycle of flux, firms are showing greater confidence to plan ahead rather than operate defensively.”

This proactive mindset is already showing up in the balance sheet. With the Federal Reserve signaling potential future rate cuts, the “window for investment and expansion is opening wider,” per Reichert. In response, CFOs are getting creative with capital, strengthening debt financing’s attractiveness and raising forecasts across the board for revenue, earnings, dividends, and even domestic hiring and wages. The businesses that move fastest to exploit this window will undoubtedly be the ones in the strongest position as conditions improve.

The Persistent Cage: Three Top Risks and a Talent Crisis

Despite the internal good cheer, the broader economic view is sobering. The North American economy is still viewed cautiously, with just 19% of CFOs viewing current conditions as “good.” The mandate for Q4, therefore, is to execute a growth strategy while navigating a minefield of systemic risk.

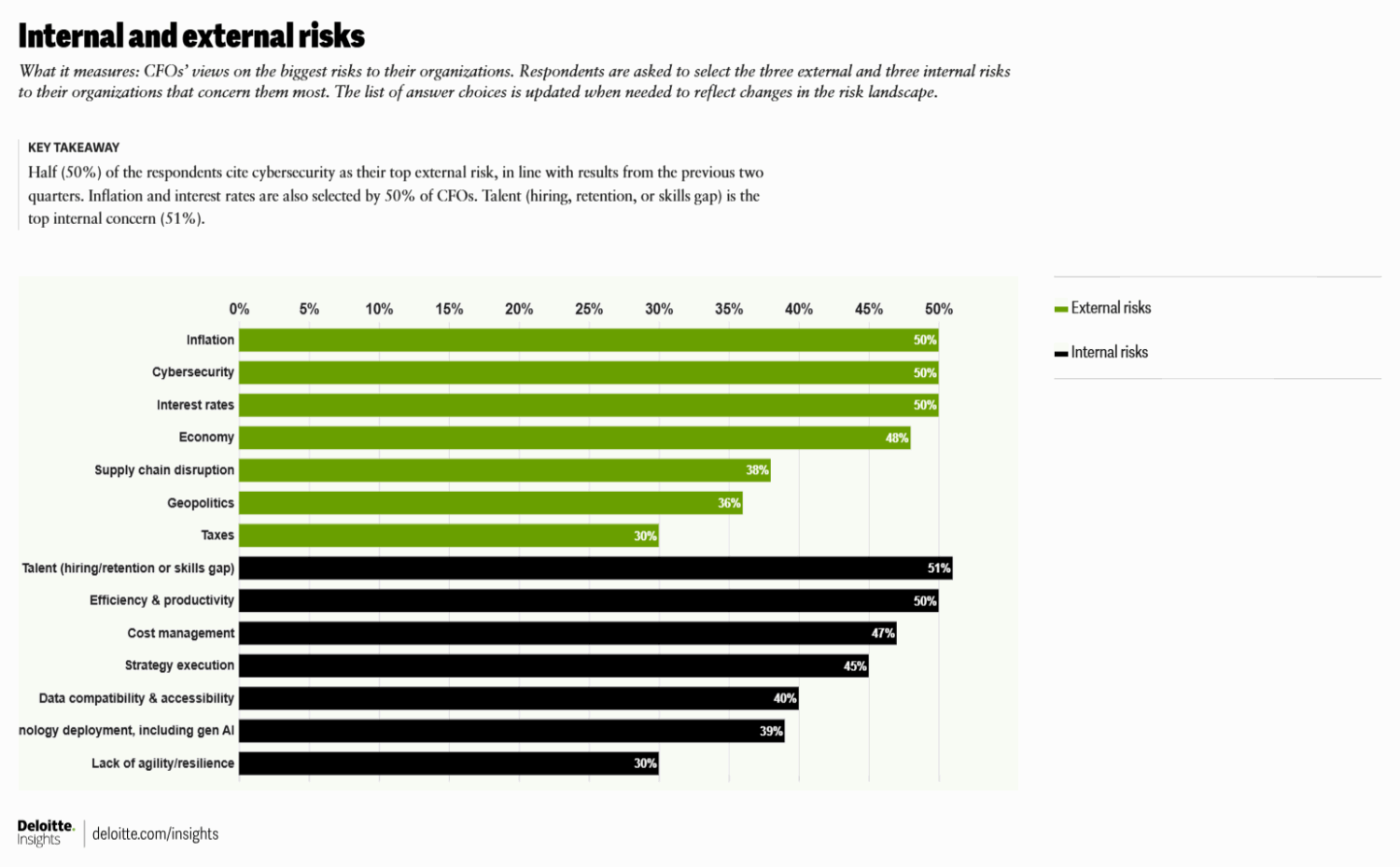

The survey highlights the three external beasts every finance team must wrestle with, all cited by 50% of respondents:

Inflation: Still on the mind, constantly eroding margins and complicating forecasting.

Interest Rates: The sword of Damocles, whose trajectory (down or up) dictates the cost of capital and the value of assets.

Cybersecurity: The modern, weaponized version of operational risk. Cyber is now a top-tier financial risk that can obliterate shareholder value in a single breach.

The irony? Even with all the external noise, the top internal risk remains the oldest one in the book: People.

In short, CFOs are confident they can find opportunities, but they aren’t confident they have the necessary talent or the cost-efficient processes to capture them.

The Global Tripwires: Trade Wars & Visa Vexations

For CFOs with international ambitions and Vistra is active in over 170 countries, advising firms on operating across markets, the policy landscape introduces two specialized, high-impact risks for Q4 and beyond that demand attention in the Boardroom.

Reichert pinpoints two areas of particular flux:

Trade & Tariffs: While the optimism rebound is a good sign, global economic policy remains in a “cycle of flux.” The specter of government efforts to rewrite trade rules and the potential legal hurdles that follow can snarl supply chains and force complex, sudden cost adjustments, undermining expansion strategies.

Talent & Visas: Directly connected to the top internal risk, shifts in key immigration areas like H-1B visas risk injecting fresh uncertainty into firms’ ability to secure specialized global talent.

The direct financial impact is not trivial. Reichert warns that companies affected by these policy shifts could face the unhappy triumvirate of “slower GDP growth, higher costs and weaker revenues.”

This is where the rubber meets the road. Nearly two-thirds (65%) of CFOs believe now is not a good time to take greater risks. The successful finance chief in Q4 won’t be the one who ignores risk, but the one who can confidently separate the necessary risks (strategic investment, M&A) from the controllable ones (compliance, operational exposure) and navigate the volatile policy risks with speed.

The direction of travel is more positive, but the journey demands precision.

The ball is now firmly in the CFO’s court: act decisively, or wait for your competitors to pass you by.